TL;DR:

- Real estate liquidity measures how quickly a property can be sold at or near its fair market value. Physical property is inherently illiquid because sales involve lengthy processes, high costs, and limited buyers, especially for luxury assets. Managing liquidity risk requires monitoring transaction volumes, maintaining capital reserves, and understanding market cycles to avoid forced sales and optimize exit strategies.

Real estate liquidity is defined as the ease and speed with which a property asset can be converted into cash at or near its fair market value. Unlike equities or bonds, physical property cannot be sold in seconds. Transaction timelines for physical real estate often span several months, requiring appraisals, title checks, and financing approvals. This structural reality shapes every investment decision in the property market, from acquisition timing to exit strategy. Understanding real estate investment liquidity is not merely academic. It is the difference between a controlled exit and a forced sale at a discount. In 2026, with transaction volumes falling sharply ahead of price adjustments, liquidity risk has moved to the centre of every serious investor’s thinking.

What is real estate liquidity and why does it matter?

Real estate liquidity describes how quickly a property can be sold without a material reduction in price. The industry term most professionals use is asset liquidity, and it sits at the heart of real estate risk assessment. A liquid asset converts to cash rapidly at close to its stated value. An illiquid asset requires time, cost, and compromise to exit.

Physical property sits firmly at the illiquid end of the spectrum. A share in Apple can be sold in milliseconds on the New York Stock Exchange. A villa in Saint-Tropez may take six to eighteen months to sell, even in a buoyant market. That gap in exit speed is the core of what real estate market liquidity measures.

The importance of liquidity in real estate extends beyond simple convenience. Illiquidity affects pricing, financing, portfolio construction, and risk management. Investors who ignore it often discover its significance at the worst possible moment, when they need capital and the market is not cooperating.

Pro Tip: When evaluating any property purchase, ask yourself how long it would realistically take to sell at full value in a flat market. That answer is your liquidity horizon, and it should inform how much of your total wealth you commit to the asset.

Why is physical property structurally illiquid?

Real estate is structurally illiquid because of the combination of high transaction costs, lengthy processes, and a limited pool of qualified buyers. Each of these factors compounds the others, creating a market where speed and certainty of sale are never guaranteed.

The transaction process creates inherent delays

Every property sale involves a sequence of steps that cannot be compressed beyond a certain point. Legal due diligence, mortgage underwriting, notarial processes in France, and title searches each take time. In France, the period between signing a compromis de vente and completing at the notaire typically runs eight to twelve weeks at minimum. Complex transactions involving foreign buyers, corporate structures, or heritage properties can extend well beyond that.

High costs reduce the pool of willing buyers

Transaction costs in real estate are substantial on both sides. In France, buyer-side notarial fees and transfer taxes typically add 7–8% to the purchase price on existing properties. These costs mean buyers require greater conviction before committing, which narrows the active market at any given moment.

The key structural factors that create illiquidity include:

- Appraisal and valuation requirements that lenders impose before releasing mortgage funds

- Legal and title checks that must be completed before contracts can exchange

- Financing approvals that depend on lender underwriting timelines, often four to eight weeks

- Property uniqueness that limits the number of buyers who will find a specific asset suitable

- Regulatory constraints on lending, including debt service coverage ratios and loan-to-value limits

Financing constraints amplify the problem

Lenders do not simply approve mortgages on request. Underwriting models assess income, debt ratios, and property valuations independently. Trailing three-month NOI averages can misrepresent current performance, complicating refinancing even when a property is performing well. This means that even a willing buyer may be unable to complete if their financing falls through, returning the property to the market and resetting the timeline entirely.

Pro Tip: For luxury property in particular, always verify that a prospective buyer has confirmed financing or demonstrable liquid assets before accepting an offer. An unqualified buyer costs you months, not weeks.

How do liquidity cycles affect real estate markets?

Real estate market liquidity is not static. It expands and contracts in cycles driven by credit availability, investor sentiment, and macroeconomic conditions. Understanding these cycles is one of the most valuable skills a property investor can develop.

The mechanics of a liquidity cycle

A liquidity cycle in real estate follows credit cycles closely. When lenders compete aggressively, loan-to-value ratios rise, financing costs fall, and transaction volumes increase. More buyers can access capital, more deals close, and markets feel liquid. When credit tightens, the reverse occurs. Buyers disappear, bid-ask spreads widen, and properties sit on the market for extended periods.

Global credit competition peaked in april 2026 driven by refinancing waves and rising lender risk tolerance. That surge in debt market activity signals an expanding liquidity phase for commercial real estate globally. The implication is that well-positioned assets with strong sponsors are finding financing more readily than at any point in recent years.

2026 liquidity conditions at a glance

| Indicator | Early 2026 Signal | Implication for Investors |

|---|---|---|

| Transaction volumes | 49% month-on-month drop in March 2026 | Exit timing risk is elevated despite stable prices |

| Debt market competition | Record highs in April 2026 | Refinancing and acquisition financing more accessible |

| Lender risk tolerance | Rising loan-to-value thresholds | Larger loan amounts available for qualifying assets |

| Price expectations | Broadly stable | Liquidity risk outpaces valuation risk in current cycle |

The March 2026 volume decline is particularly instructive. Prices held steady while transaction volumes collapsed. This is the classic signature of a liquidity contraction: sellers hold firm on price, buyers retreat, and the market freezes. Volume is the honest signal. Price is the lagging one.

Marketability is not the same as liquidity

Geoffrey Dohrmann, a recognised authority on real estate investment, draws a sharp distinction between marketability and liquidity. A property may be marketable, meaning it will eventually sell, without being liquid, meaning it cannot be converted to cash quickly at fair value. Confusing the two leads investors to underestimate their true exit risk. A prestige villa in Cannes will always find a buyer eventually. Whether it finds one in thirty days at asking price is an entirely different question.

Pro Tip: Track transaction volumes in your target market, not just listing prices. Volumes tell you how liquid the market actually is. Prices tell you what sellers wish were true.

How does liquidity differ across real estate asset types?

Real estate asset liquidity varies enormously depending on the type of asset, its location, and the structure through which it is held. Investors who treat all property as equally illiquid miss important distinctions that affect portfolio construction and risk.

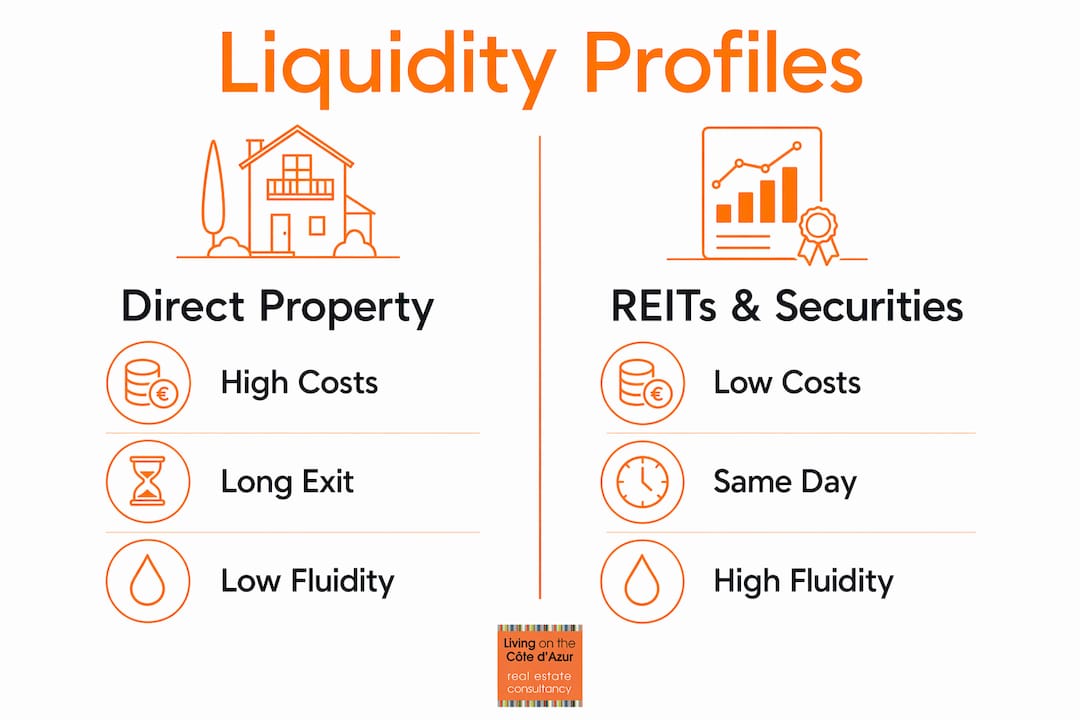

Direct property versus reits and securitised products

The most liquid form of real estate investment is the Real Estate Investment Trust, or REIT. Shares in listed REITs such as Unibail-Rodamco-Westfield or Gecina trade on public exchanges and can be bought or sold within a trading day. The underlying assets are still illiquid buildings, but the securitised wrapper provides daily liquidity. The trade-off is that REIT prices correlate more closely with equity markets, reducing the diversification benefit that direct property provides.

Direct physical property sits at the opposite end. A commercial office building in Paris or a luxury residence in Monaco requires months to transact and carries substantial transaction costs on both entry and exit. The illiquidity premium that direct property offers, in the form of higher long-term returns and reduced short-term volatility, compensates patient investors for accepting that illiquidity.

Comparing liquidity profiles across asset classes

| Asset Type | Typical Exit Timeline | Transaction Costs | Liquidity Profile |

|---|---|---|---|

| Listed REITs | Same day | Low (brokerage fees) | High |

| Residential property (standard) | Three to six months | Moderate (5–8%) | Moderate |

| Commercial property | Six to eighteen months | High (8–12%) | Low |

| Luxury and trophy assets | Twelve to thirty-six months | High (8–12%) | Very low |

| Off-market luxury property | Variable, buyer-dependent | Negotiated | Specialist |

The luxury segment requires particular attention

Luxury and off-market properties present a distinct liquidity profile. The buyer pool is global but narrow. A property priced above €5 million in Saint-Tropez or Monaco competes for a small number of qualified buyers worldwide. This concentration of demand means that factors driving liquidity variations between asset types are amplified at the prestige end of the market.

Financing differences between commercial and residential assets also affect liquidity. Commercial loan structures differ materially from residential mortgages in terms of underwriting criteria, rate structures, and covenant requirements. These differences shape how quickly buyers can complete and therefore how liquid the market is at any given moment.

Key distinctions for investors to hold in mind:

- Residential property in established urban markets is more liquid than commercial or rural assets

- Luxury property commands a premium but accepts a narrower buyer pool and longer exit timelines

- Off-market transactions can accelerate exits for the right asset with the right network

- Securitised real estate products offer liquidity at the cost of direct ownership benefits

How can investors assess and manage real estate liquidity risk?

Managing real estate investment liquidity risk requires discipline, data, and a clear-eyed view of your own financial position. The investors who suffer most in illiquid markets are those who needed to sell before they were ready to accept the market’s terms.

Private capital experts define liquidity as access to cash or credit lines to prevent distressed sales. This definition shifts the focus from the asset itself to the investor’s balance sheet. You can own a perfectly sound property and still face a liquidity crisis if you have no reserves and the market stalls.

A practical framework for assessing liquidity

Follow these steps to build a clear picture of your liquidity position before and after any property acquisition:

- Track transaction volumes, not just prices. Low transaction volume despite high listing prices signals liquidity risk. Actual sales data is the only reliable indicator of market depth.

- Assess time-on-market for comparable properties. If similar assets in your target area are sitting unsold for twelve months or more, your exit timeline should reflect that reality.

- Monitor bid-ask spreads. A widening gap between asking prices and achieved sale prices indicates a market where sellers and buyers disagree on value. That disagreement freezes transactions.

- Evaluate your financing position independently. Do not assume that refinancing will be available when you need it. Lenders favour borrowers who maintain assets and expense ratios carefully, even in liquidity-rich markets.

- Maintain a liquidity buffer. Hold cash or credit facilities equivalent to at least twelve months of carrying costs for each property. This prevents a temporary market freeze from becoming a forced sale.

- Time acquisitions to the cycle. Buying during a liquidity contraction, when volumes are low and sentiment is cautious, often produces better entry prices. Selling during an expansion phase, when credit is flowing and buyers are active, maximises exit values.

Common pitfalls to avoid

Relying on listing prices rather than transaction data is the most common error. A market can appear active based on new listings while actual completions collapse. The March 2026 volume data illustrates this precisely: prices looked stable while the real market was seizing up.

Sophisticated liquidity assessment looks beyond listing activity to actual transactional data and lender behaviour. Investors who track only asking prices are navigating with an incomplete map. The step-by-step transaction process for luxury real estate makes clear just how many points of failure exist between offer and completion.

Key takeaways

Real estate liquidity is the defining risk factor that separates property investment from all other asset classes, and managing it requires monitoring transaction volumes, maintaining capital reserves, and understanding where you sit in the liquidity cycle.

| Point | Details |

|---|---|

| Liquidity defines exit risk | Property cannot be sold quickly at fair value; timelines of months to years are normal. |

| Cycles drive market conditions | Transaction volumes, not prices, are the honest signal of real estate market liquidity. |

| Asset type determines profile | REITs offer daily liquidity; direct luxury property may take years to exit at full value. |

| Investor balance sheet matters | Access to cash or credit lines prevents forced sales during market contractions. |

| Marketability is not liquidity | A property that will eventually sell is not liquid unless it converts to cash quickly at fair value. |

Why liquidity is the risk most investors underestimate

I have spent years working with discerning buyers and investors across the Côte d’Azur, and the pattern I see most consistently is this: investors who have made their wealth in equities or business underestimate how different illiquidity feels when it is your capital that is locked in.

In equities, a bad position can be exited in seconds. In property, a bad position can take two years to resolve, and every month of carrying costs erodes your return. The illiquidity premium that direct real estate offers is real and meaningful. But it is only a premium if you have the financial resilience to hold through a cycle without being forced to sell.

The 2026 market has reinforced this lesson sharply. The March volume collapse, with a 49% month-on-month drop in transactions, caught many investors off guard precisely because prices had not moved. They assumed a stable price meant a liquid market. It did not. Liquidity had already evaporated. Price was simply the last thing to reflect it.

My contrarian view is that illiquidity, properly understood, is not a flaw in real estate. It is a feature. The friction that slows transactions also prevents the panic-driven volatility that destroys value in public markets. The investors who build wealth in property are those who embrace the illiquidity, plan for it, and use it to their advantage by buying when others cannot and holding when others must sell.

The mistake is not owning illiquid assets. The mistake is owning them without the liquidity buffer to survive a cycle.

— Ab Kuijer

Discover prestige properties where liquidity meets opportunity

At Livingonthecotedazur, we work with investors who understand that the finest properties on the Côte d’Azur are rarely found on public portals. Our curated access to off-market luxury properties across Saint-Tropez, Monaco, Cannes, and Cap d’Antibes means you see assets before they reach the open market, where competition is lower and negotiation is more favourable. We also provide comprehensive support on luxury property financing and due diligence, so that every acquisition is structured to protect both your capital and your exit options. If you are ready to invest with clarity and confidence, we are here to guide you.

FAQ

What is real estate liquidity in simple terms?

Real estate liquidity is how quickly and easily a property can be sold at close to its market value. Physical property is considered illiquid because sales typically take months and involve significant costs.

Why is real estate less liquid than stocks or bonds?

Property requires appraisals, legal checks, financing approvals, and a willing qualified buyer, all of which take time. Stocks trade on exchanges in seconds; property transactions in France alone typically take eight to twelve weeks from offer to completion.

What is the difference between liquidity and marketability in real estate?

Marketability means a property will eventually find a buyer. Liquidity means it can be converted to cash quickly at fair value. As Geoffrey Dohrmann notes, a property can be marketable without being liquid, and confusing the two leads investors to underestimate their exit risk.

How can i assess real estate liquidity before buying?

Track actual transaction volumes and time-on-market data for comparable properties in your target area, not just listing prices. Low volumes alongside high asking prices signal a market where exits will be slow and costly.

Does illiquidity always hurt real estate investors?

Not necessarily. Illiquidity acts as a market stabiliser, reducing the flash volatility seen in public markets and rewarding patient investors with an illiquidity premium over time. The risk arises when investors lack the capital reserves to hold through a contraction without being forced to sell.

Recommended

//

//