TL;DR:

- Choosing the right ownership structure, such as LLCs, trusts, or joint tenancy, is essential before signing a property contract to ensure proper legal and tax planning. Effective financing methods, like DSCR loans or conventional mortgages, should match the property’s type and your investment goals to optimize costs and speed. Thorough preparation, including forming entities early and verifying details at closing, prevents costly delays and safeguards your investment.

Structuring a property purchase is defined as the deliberate process of selecting the right ownership vehicle, financing method, and legal framework before signing any contract. The decisions you make at this stage determine your tax exposure, legal protection, financing costs, and long-term flexibility. Most buyers focus on finding the right property. The buyers who build lasting wealth focus equally on how they hold and finance it. This guide walks you through every layer of the property acquisition process, from choosing your ownership structure to closing securely, with the clarity and precision that a decision of this magnitude deserves.

How to structure a property purchase: ownership options explained

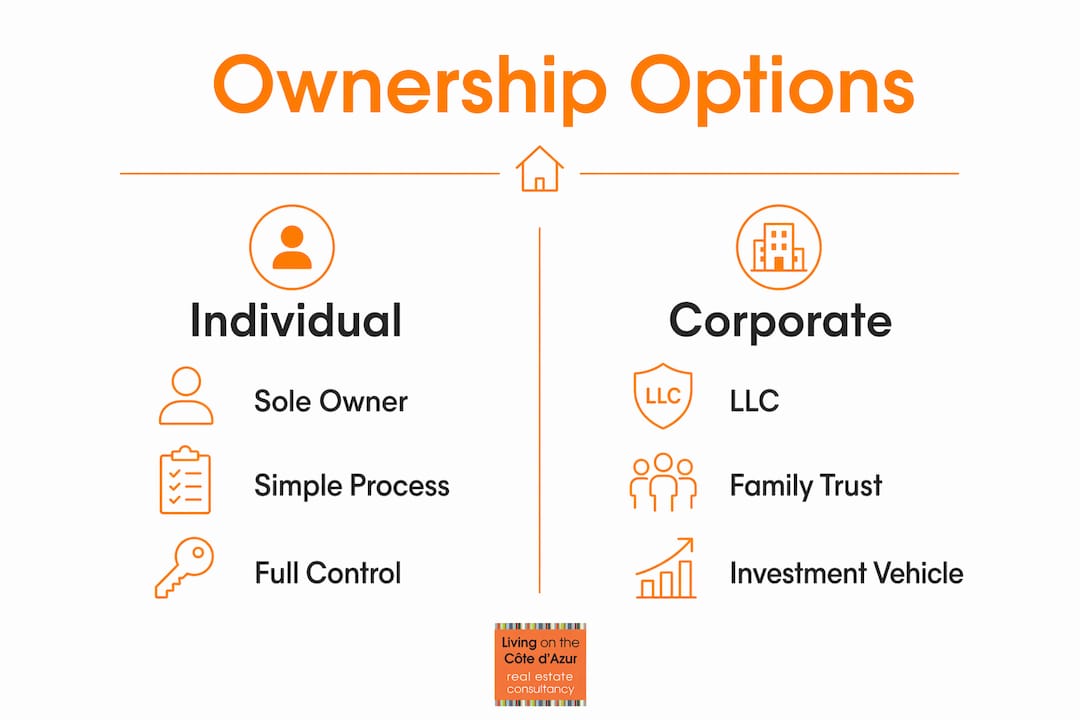

The ownership structure you choose is not a formality. It is the legal and financial foundation of your entire investment. The four primary options are individual ownership, joint tenancy, family trusts, and limited liability companies (LLCs). Each carries distinct implications for tax, succession, and legal protection.

Individual ownership places the property solely in your name. It is the simplest arrangement and suits buyers purchasing a primary residence with no plans to expand a portfolio. The drawback is full personal liability. If the property generates a dispute or debt, your personal assets are exposed.

Joint tenancy is the standard choice for couples and co-buyers. It includes the right of survivorship, meaning the surviving owner inherits the deceased partner’s share automatically, bypassing probate. This is particularly relevant for families purchasing legacy properties in France, where succession law can otherwise complicate transfers.

Family trusts add a layer of estate planning sophistication. A trust holds the property on behalf of named beneficiaries, separating legal ownership from beneficial ownership. This structure is favoured by high-net-worth families who want to pass assets across generations without triggering unnecessary tax events or probate delays.

LLCs are the preferred vehicle for buyers acquiring income-generating or investment properties. An LLC separates your personal finances from the property’s liabilities entirely. One critical rule applies here: form the LLC before signing the purchase contract. Attempting to assign a contract to an entity formed after signing creates title discrepancies and costly amendments that can derail the transaction.

The factors that should guide your choice include your tax residency, the number of co-buyers, your succession intentions, and whether you plan to hold one property or build a portfolio. A family buying a second home on the Côte d’Azur for personal use has very different structural needs from an investor acquiring a rental villa in Saint-Tropez.

Pro Tip: If you are considering an LLC or any corporate vehicle, instruct your solicitor to confirm the entity is in good standing before the contract is drafted. A single missed filing can put the entire transaction on hold.

How do you finance a property purchase effectively?

Financing is where most buyers lose money, not through bad rates, but through mismatched capital. Matching financing to the asset and your business plan produces better outcomes than chasing the lowest interest rate alone.

Conventional mortgages

Conventional mortgages remain the benchmark for primary residence buyers. They typically require a down payment of 20–25% with interest rates in the 4–5% range. That lower rate comes with stricter income verification, longer underwriting timelines, and lender scrutiny of your personal financial profile. For a family buying a curated family home, this is usually the right tool.

DSCR loans

Debt Service Coverage Ratio (DSCR) loans evaluate the property’s rental income rather than your personal income. They require a minimum 20% deposit but carry rates of 6–8% and close in as few as 15–21 days. The speed and income-agnostic qualification make DSCR loans particularly powerful for buyers acquiring multiple properties without wanting each purchase to trigger a full personal income audit. For portfolio builders, this is the structure that enables scale.

Alternative financing

Hard money loans and bridge loans serve a specific purpose: speed and flexibility when a property’s condition or timeline makes conventional lending impractical. Hard money lenders focus on the asset’s value rather than your creditworthiness. Bridge loans cover the gap between purchasing a new property and selling an existing one. Both carry higher rates and shorter terms, so they suit short-term holds or renovation projects, not long-term ownership.

Comparing your financing options

| Financing Type | Down Payment | Interest Rate | Closing Speed | Best For |

|---|---|---|---|---|

| Conventional Mortgage | 20–25% | 4–5% | 30–45 days | Primary residence, strong income profile |

| DSCR Loan | 20%+ | 6–8% | 15–21 days | Rental properties, portfolio growth |

| Hard Money Loan | 25–35% | 9–12%+ | 7–14 days | Distressed assets, short-term holds |

| Bridge Loan | Varies | 7–10% | 10–21 days | Transitional purchases, renovation projects |

Pro Tip: Before committing to any financing type, calculate your total cost of capital over the full hold period, not just the headline rate. A DSCR loan at 7% that closes in 15 days may cost less overall than a conventional mortgage at 4.5% that takes 60 days and causes you to miss the property.

For buyers considering luxury property financing on the French Riviera, local lenders and international private banks often offer bespoke terms that do not appear in standard comparison tables.

What are the steps to buy a house from offer to closing?

The full property purchase process runs from 3 to 6 months in total, with the formal contract-to-close period lasting 30–45 days. Understanding each phase prevents costly surprises and keeps your transaction on schedule.

The chronological purchase process

Secure pre-approval. Before viewing properties, obtain a mortgage pre-approval or proof of funds. This defines your budget with precision and signals credibility to sellers in competitive markets.

Define your structure. Decide on your ownership vehicle and confirm your financing type before making any offer. Changing these after offer acceptance creates delays and can cost you the property.

Make your offer. Submit a written offer with your proposed price, contingencies, and earnest money deposit. Earnest money typically ranges from 1–3% of the purchase price and is credited toward your down payment or closing costs at completion.

Negotiate contingencies. Standard contingencies include financing, survey, and inspection. Each one protects you but also signals caution to the seller. In a strong market, a bloated contingency package weakens your position.

Execute the contract. Once both parties sign, the formal closing period begins. Your solicitor or notaire reviews title, confirms the ownership structure is correctly documented, and manages the transfer of funds.

Close the transaction. Final funds transfer, title is recorded, and keys are exchanged. This is also the stage where wire fraud risk peaks.

Documents you will need

- Proof of identity and residency

- Mortgage pre-approval or proof of funds letter

- LLC or trust formation documents (if applicable)

- Survey and inspection reports

- Title insurance commitment

- Signed purchase contract with all addenda

Common pitfalls at closing

- Sending wire transfers without verbally confirming bank details directly with your solicitor. Closing scams targeting buyers have increased significantly, with fraudsters intercepting email communications to redirect funds.

- Arriving at closing without sufficient liquid reserves. Closing costs typically add 2–5% to your total outlay beyond the deposit.

- Failing to review the final settlement statement before the closing date. Errors in figures are not uncommon and are far easier to correct before signing than after.

For a detailed walkthrough of the luxury transaction process, the legal steps in France carry additional nuance, particularly around the notaire’s role and the compromis de vente.

What mistakes derail a property purchase structure?

The most expensive errors in property acquisition are structural, not financial. They happen before the first offer is made, and they compound throughout the transaction.

The most common structural errors

Signing before forming your entity. Buyers who intend to purchase through an LLC but sign the contract in their personal name face a difficult choice: proceed personally or attempt a costly contract amendment. Title discrepancies from this error can delay closing by weeks or invalidate the transaction entirely.

Overloading contingencies in a competitive market. Too many contingencies weaken your offer in fast-moving markets, while too few leave you legally exposed. The right balance depends on local market velocity and the specific property’s condition.

Underestimating liquidity at closing. Buyers often calculate the deposit and forget closing costs, legal fees, survey fees, and the first tranche of ownership costs. Arriving at closing underfunded is one of the most avoidable disasters in the property buying process.

Choosing financing based on rate alone. A lower rate on a financing product that does not suit the property’s condition or your timeline will cost more in the end. A property requiring renovation will not qualify for conventional financing, regardless of your credit profile.

Ignoring title discrepancies. Title issues discovered late in the process can be renegotiated, but only if you have a solicitor reviewing the title commitment early. Buyers who skip this step often discover problems on the day of closing.

Pro Tip: When submitting your earnest money deposit, use a precise, non-rounded figure. A specific deposit amount signals to the seller that you have done rigorous analysis on the property’s value, not simply guessed a round number. This small detail differentiates serious buyers from casual ones.

You can explore the property acquisition process in greater depth, including how to approach due diligence on prestige properties where title history and planning permissions require specialist review.

Key takeaways

A well-structured property purchase integrates the right ownership vehicle, matched financing, and disciplined legal execution from the very first step.

| Point | Details |

|---|---|

| Choose ownership structure first | Select individual, joint tenancy, trust, or LLC before making any offer. |

| Form legal entities before signing | An LLC or trust must be established and in good standing prior to contract execution. |

| Match financing to the asset | Conventional mortgages suit primary residences; DSCR loans suit portfolio growth and faster closings. |

| Use earnest money strategically | A precise, non-rounded deposit signals serious intent and rigorous due diligence to sellers. |

| Protect yourself at closing | Verify all wire transfer details by telephone and review the settlement statement before signing day. |

What i have learnt from watching buyers get this wrong

By Ab Kuijer

After years of guiding discerning buyers through property acquisitions on the Côte d’Azur and beyond, the pattern I see most consistently is this: buyers invest enormous energy in finding the right property and almost none in deciding how to hold it. The ownership structure conversation happens as an afterthought, usually prompted by a solicitor at the contract stage, when the options have already narrowed.

The buyers who build genuine, lasting wealth from property treat the structure as the first decision, not the last. They arrive at the negotiating table knowing whether they are buying personally, through a family trust, or via a corporate vehicle. They have spoken to a tax adviser and a succession specialist before they have spoken to a mortgage broker. That sequence matters enormously.

On the financing side, I have watched buyers dismiss DSCR loans because the rate looks higher on paper. What they miss is that DSCR financing can close in under three weeks, bypasses personal income scrutiny, and allows them to acquire a second or third property without waiting for a conventional lender to re-underwrite their entire financial life. For families building a portfolio across France and Ibiza, that speed and flexibility is worth far more than a 1.5% rate differential.

The security point deserves more attention than it typically receives. Wire fraud at closing is not a theoretical risk. It is an active and growing threat. I recommend that every buyer establish a verbal confirmation protocol with their solicitor before any funds move. No email instruction alone should ever trigger a transfer.

My honest counsel is this: spend as much time choosing your structure as you spend choosing your property. The property you can always sell. A poorly chosen structure can follow you for decades.

— Ab Kuijer

Discover prestige properties on the côte d’azur

At Livingonthecotedazur, we work with individuals and families who understand that the finest properties rarely appear on public listings. Our access to exclusive off-market properties across Saint-Tropez, Monaco, and the wider Riviera gives our clients a distinct advantage in one of the world’s most coveted markets. We pair that access with specialist guidance on ownership structuring, tax optimisation, and financing, so that every acquisition is as sound in its architecture as it is beautiful in its setting. If you are ready to explore what is genuinely available, we invite you to begin your search with us. The right property, held in the right structure, is a legacy worth building.

FAQ

What does structuring a property purchase mean?

Structuring a property purchase means choosing the ownership vehicle, financing method, and legal framework before signing any contract. The goal is to align the acquisition with your tax position, succession plans, and long-term financial objectives.

When should i form an LLC before buying property?

The LLC must be formed and in good standing before the purchase contract is signed. Signing in your personal name and attempting to transfer to an entity afterwards creates title discrepancies and can delay or derail the closing.

What is a DSCR loan and who is it for?

A DSCR loan qualifies based on the property’s rental income rather than your personal income, with rates of 6–8% and closing times as short as 15–21 days. It suits investors building a portfolio who want to avoid repeated personal income verification.

How much earnest money should i offer?

Earnest money deposits typically range from 1–3% of the purchase price. Using a precise, non-rounded figure signals to the seller that your offer is based on thorough analysis rather than a casual estimate.

How long does the full property purchase process take?

The complete process from initial search to closing typically takes 3–6 months. The formal contract-to-close period alone runs 30–45 days, depending on financing type, title complexity, and local market conditions.

Recommended

//

//