TL;DR:

- An investment property is real estate purchased primarily for income or capital appreciation, not personal use. Its classification depends on intent, affecting financing, taxation, and reporting standards. Strategic location, tenant demand, and accurate financial modeling are essential for successful Riviera investments.

An investment property is real estate purchased primarily to generate income or capital appreciation, not to serve as the buyer’s personal residence. This distinction, simple on the surface, carries profound implications for financing terms, tax treatment, accounting classification, and long-term wealth strategy. Whether you are considering a sun-drenched villa above Cannes, a polished apartment in Nice’s Mont Boron quarter, or a stone-built mas in the hills above Grasse, understanding the investment property definition is the foundation upon which every sound acquisition decision rests. The Côte d’Azur, with its constellation of prestigious villages and year-round tourism, offers one of Europe’s most compelling arenas for this pursuit.

What is an investment property and how is it defined?

An investment property is real estate bought to earn returns through rental income, capital appreciation, or both, rather than for personal occupancy. The classification hinges entirely on intent. Two physically identical villas in Beaulieu-sur-Mer may be treated entirely differently under law and accounting standards depending solely on whether the owner lives in one or holds the other for gain.

Under IAS 40, the international accounting standard adopted across IFRS jurisdictions, investment property is formally defined as land or buildings held to earn rentals or for capital appreciation, explicitly excluding owner-occupied properties and those held for sale in the ordinary course of business. This matters because IAS 40 dictates separate measurement and disclosure rules, which affect how investors and companies report asset values on their balance sheets. For private buyers, the practical consequence is that your lender, your accountant, and the French tax authority will each treat the property according to this same underlying logic of intent.

The investment property label is about purpose, not physical features. A two-bedroom apartment in Saint-Paul-de-Vence rented to visiting art collectors during the summer season qualifies. The same apartment occupied by its owner does not. This clarity of purpose also shapes your entire financial strategy from day one.

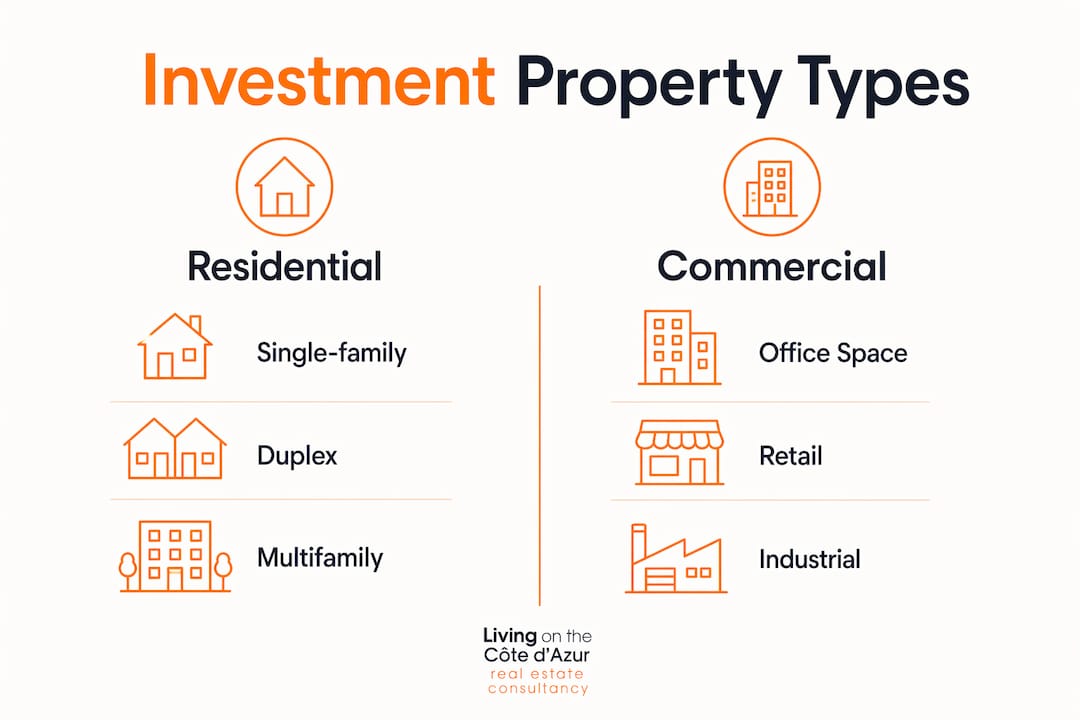

What types of properties qualify as investment properties?

Investment properties span a broad spectrum, and understanding the types of real estate investments available helps you match asset class to strategy. The primary categories are residential, commercial, and mixed-use, each carrying distinct risk profiles and return characteristics.

| Property type | Primary return driver | Côte d’Azur example |

|---|---|---|

| Single-family rental | Steady rental income | Villa in Mougins let to long-term tenants |

| Multi-unit residential | Diversified rental income | Apartment building in Cagnes-sur-Mer |

| Vacation or short-term rental | Premium seasonal yield | Sea-view apartment in Cannes |

| Commercial | Lease income, capital gain | Boutique retail in Antibes old town |

| Off-plan new build | Capital appreciation on completion | VEFA apartment in Sainte-Maxime |

Residential investment properties, including single-family rentals, duplexes, multifamily homes, and condominiums, represent the most accessible entry point for individual investors and families. Vacation rentals occupy a particularly lucrative niche on the Riviera, where short-term demand from the Cannes Film Festival circuit, Monaco Grand Prix visitors, and the summer influx along the Croisette commands premium nightly rates. Commercial properties, by contrast, tend to attract institutional capital and require deeper market knowledge, though boutique retail or hospitality assets in villages like Èze or Valbonne can deliver attractive lease income.

The critical distinction from owner-occupied real estate is intent and use. A property you purchase in Roquebrune-Cap-Martin and use personally for more than a defined threshold of days per year may lose its investment classification for tax purposes, reducing the deductions available to you. Structuring ownership and use correctly from the outset protects both your returns and your compliance.

How is buying an investment property financed?

Financing an investment property operates under stricter conditions than a primary residence mortgage, and understanding these differences prevents costly surprises. Lenders regard investment loans as higher risk because borrowers are more likely to default on a property they do not live in during financial stress.

Key financing realities to prepare for:

- Down payment. Investment property loans typically require around 25% down, compared with 5 to 10% for owner-occupied purchases. On a €2 million villa in Cap-d’Ail, that represents €500,000 in equity before the transaction completes.

- Credit profile. Lenders generally require a credit score of 620 or above, though prime Riviera lenders and private banks serving high-net-worth clients apply their own bespoke criteria.

- Debt-service coverage. Underwriters assess whether projected rental income covers the mortgage payment, typically requiring a ratio above 1.25.

- Bridging finance. For off-plan acquisitions under VEFA contracts in Sainte-Maxime or Nice, bridging loans allow buyers to secure the asset before long-term mortgage drawdown, a common structure for new-build purchases.

- Cryptocurrency-backed financing. Livingonthecotedazur accepts cryptocurrency payments, opening a pathway for digital-asset holders to convert portfolio gains directly into Riviera stone without liquidating through traditional banking channels.

Ongoing expenses demand equal rigour. Property management fees, maintenance reserves, local taxe foncière, co-ownership charges, and insurance all reduce net income. Rental income and expenses affect tax reporting directly, and the classification of your property as an investment asset unlocks deductible expenses unavailable to owner-occupiers.

Pro Tip: Before approaching any lender, prepare a detailed income projection for the property, including realistic vacancy assumptions. A well-documented dossier signals sophistication and accelerates approval, particularly with French private banks accustomed to international buyers.

How to evaluate the performance of an investment property

Performance evaluation separates disciplined investors from optimistic buyers. Three metrics form the analytical core of any credible property assessment.

- Net operating income (NOI). NOI is calculated as gross rental income minus all operating expenses, excluding mortgage payments. If a Cannes apartment generates €80,000 per year in rent and incurs €25,000 in operating costs, the NOI is €55,000.

- Capitalisation rate (cap rate). Divide NOI by the purchase price. A €55,000 NOI on a €1.1 million property produces a cap rate of 5%, which sits comfortably within the 3 to 5% annual yield range typical of elite Riviera lets.

- Cash-on-cash return. Divide annual pre-tax cash flow (after mortgage payments) by the total cash invested. This metric reflects the actual return on your deployed capital, not the asset’s total value.

| Metric | Formula | Example result |

|---|---|---|

| NOI | Gross income minus operating expenses | €55,000 |

| Cap rate | NOI divided by purchase price | 5% |

| Cash-on-cash return | Annual cash flow divided by cash invested | 7.2% |

Vacancy rates and operating expenses must be modelled realistically. Ignoring a 10% vacancy assumption on a seasonal rental in Menton, where the Lemon Festival and summer tourism drive occupancy peaks but winter months soften demand, leads to failed underwriting and negative cash flow. The luxury rental investment workflow we recommend accounts for these seasonal rhythms explicitly.

Pro Tip: Run your numbers at 80% occupancy, not 100%. If the investment still works at that level, you have built in a genuine margin of safety. If it only works at full occupancy, the risk profile is higher than it appears.

What makes a good investment property on the Côte d’Azur?

Good investment properties align with investor goals. Those focused on cash flow prioritise steady rental demand; those building generational wealth target capital appreciation in prestige locations. The Côte d’Azur villages serve both strategies with rare elegance.

The qualities that define a sound acquisition include:

- Location with enduring desirability. Saint-Jean-Cap-Ferrat, consistently ranked among Europe’s most exclusive addresses, commands €2M-plus premiums for sea-view properties and has appreciated reliably over decades.

- Tenant demand depth. Nice, with its international airport, university population, and year-round cultural calendar anchored by the Cours Saleya flower market and Château Hill panoramas, sustains rental demand across all seasons.

- Infrastructure and connectivity. Villages like Valbonne and Mougins, set in the Sophia Antipolis technology corridor, attract corporate tenants and digital professionals seeking Provençal lifestyle without sacrificing connectivity.

- Cultural and event magnetism. Communities like Cannes, Nice, and Saint-Paul-de-Vence host events that sustain strong rental markets throughout the year. In late July 2026, the Cannes Yachting Festival preparation period drives premium short-term demand along the Croisette, while Menton’s summer concerts at the Parvis de la Basilique Saint-Michel fill the village with cultured visitors who become ideal short-term tenants.

- Growth prospects and new supply constraints. Théoule-sur-Mer and Mandelieu-la-Napoule benefit from protected coastline that limits new development, preserving the scarcity premium that underpins long-term appreciation.

“The finest investment properties on the Riviera are not merely assets. They are heirlooms that pay their own way, places where the salt-kissed air and lavender-laced breezes are part of the return on capital.” — Livingonthecotedazur

The prime investment property examples we curate across these villages reflect this philosophy. From restored Provençal mas above Grasse, where the perfume capital’s heritage draws visitors to the annual Fête de la Rose each May, to off-plan sea-view apartments in Sainte-Maxime where Nartelle beach sunsets and the ferry to Saint-Tropez make every weekend an adventure, the Riviera offers a depth of choice that few markets can rival. Explore investment strategies for legacy and yield to understand how these locations fit within a broader wealth architecture.

Key takeaways

An investment property generates returns through rental income or capital appreciation, and its classification by intent determines every financial, legal, and tax consequence that follows.

| Point | Details |

|---|---|

| Definition by intent | A property is classified as an investment asset based on purpose, not physical features. |

| Financing is stricter | Expect around 25% down payment and rigorous credit assessment for investment loans. |

| Three core metrics | NOI, cap rate, and cash-on-cash return are the essential tools for evaluating any acquisition. |

| Riviera villages outperform | Locations like Cannes, Nice, and Saint-Jean-Cap-Ferrat combine yield with long-term appreciation. |

| Seasonal modelling matters | Realistic vacancy assumptions protect cash flow in markets with peak and off-peak demand cycles. |

Why intent matters more than most investors realise

Having worked with buyers across the Côte d’Azur for years, the single most consistent mistake I observe is purchasing a property with vague intentions. Buyers who tell themselves they will “use it sometimes and rent it the rest of the time” often end up with an asset that qualifies for neither the full tax benefits of an investment property nor the lifestyle satisfaction of a true second home. The two-part classification test of income-generation purpose and separation from personal use is not bureaucratic pedantry. It is the architecture of your entire financial strategy.

The Riviera market rewards clarity. Investors who commit to a defined exit strategy, whether that is a 10-year hold with seasonal letting in Roquebrune-Cap-Martin or an off-plan purchase in Beausoleil for capital gain on completion, consistently outperform those who leave their intentions ambiguous. I have also seen buyers underestimate the carrying costs of prestige properties. A magnificent estate above Èze, where Nietzsche once walked and the pebbled coves shimmer below, still requires property management, maintenance, and tax compliance. Build those costs into your model before you fall in love with the view.

The Riviera is genuinely one of the world’s most resilient luxury property markets. But resilience rewards the prepared. Engage a notaire early, commission an independent technical survey, and model your returns at conservative occupancy levels. The properties that appreciate 5 to 8% annually and deliver 3 to 5% rental yields are real. They simply require the discipline to find and structure them correctly.

— ab

Discover curated investment properties with Livingonthecotedazur

Livingonthecotedazur specialises in connecting discerning global buyers with the finest investment-grade real estate across the Côte d’Azur’s most prestigious villages, from the lemon-scented lanes of Menton to the yacht-dotted marinas of Antibes. Our portfolio spans off-market estates, new-build VEFA opportunities with 10-year warranties and lower notary fees, and legacy properties designed to generate income across generations. We accept cryptocurrency payments, offering digital-asset investors a direct route into Riviera stone. Whether you are seeking a seasonal rental asset in Cannes or a generational holding in Saint-Jean-Cap-Ferrat, explore our luxury investment property selection or discover off-market Riviera properties available exclusively through our network.

FAQ

What is the investment property definition in simple terms?

An investment property is real estate bought to generate income or profit rather than to live in. Common forms include rental homes, holiday lets, and commercial premises held for capital gain.

How much deposit is needed for an investment property?

Investment property loans typically require around 25% as a down payment, compared with lower thresholds for owner-occupied mortgages. Lenders apply stricter underwriting because the perceived default risk is higher.

What makes a good investment property on the French Riviera?

Location, tenant demand, and scarcity of supply are the defining factors. Villages like Cannes, Nice, Saint-Jean-Cap-Ferrat, and Valbonne combine year-round rental demand with constrained new supply, supporting both yield and long-term appreciation.

How is investment property performance measured?

The three primary metrics are net operating income, capitalisation rate, and cash-on-cash return. Together they reveal whether a property generates genuine profit after all realistic costs and vacancy periods are accounted for.

Can I buy an investment property on the Côte d’Azur using cryptocurrency?

Yes. Livingonthecotedazur accepts cryptocurrency payments, making it possible for digital-asset holders to acquire Riviera investment properties without routing capital through traditional banking channels. Contact the team directly to discuss structuring options.

Recommended

//

//