TL;DR:

- Owning a second home on the Côte d’Azur involves complex tax, legal, and inheritance considerations.

- Rental activity and commune location significantly influence tax obligations and legacy planning strategies.

- Viewing secondary residences as legacy assets, not just vacation homes, maximizes long-term wealth benefits.

Owning a second property on the Côte d’Azur conjures images of cerulean seas, the scent of lavender drifting over Cap d’Antibes, and mornings spent watching yachts glide past Cannes’ Croisette. Yet beneath that salt-kissed allure lies a legal and fiscal architecture that surprises even seasoned global investors. A secondary residence in France is not simply a holiday address. It carries specific tax obligations, commune-level rules, and legacy implications that shape the true cost and opportunity of ownership. Understanding these nuances is not optional; it is the foundation of every intelligent Riviera acquisition.

Table of Contents

- Defining secondary residence: More than a second home

- Personal use, rental, and tax categorisation: Navigating dual roles

- French Riviera commune taxes: Local nuances every investor should know

- Acquisition strategies for secondary residences: Personal enjoyment and legacy investment

- A fresh perspective: Redefining secondary residence for legacy investors

- Explore luxury Riviera real estate opportunities

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Beyond holiday use | Secondary residences require more than personal enjoyment—they carry legal and tax consequences that affect legacy planning. |

| Tax categorisation matters | How you use and declare your property determines its tax treatment and influences future returns. |

| Local rules impact | French Riviera commune taxes and local surcharges must be understood for effective investment. |

| Strategic acquisition | Successful investors balance lifestyle goals with tax and legacy outcomes when acquiring a secondary residence. |

| Legacy-first mindset | Reframing secondary residence decisions with generational wealth and compliance in mind yields superior long-term results. |

Defining secondary residence: More than a second home

The term “secondary residence” sounds straightforward. In practice, it is one of the most consequential legal classifications a property owner on the French Riviera will encounter. French law defines a secondary residence as any property that is not your principal habitation, meaning the dwelling where you reside for the majority of the calendar year. Everything else, whether a sun-drenched villa above Èze or a sleek penthouse near the Monaco border, falls into the secondary category.

This distinction matters enormously because second home taxes in France operate within a domestic tax and occupancy categorisation framework, not an immigration status framework. Many international buyers arrive believing their Riviera property qualifies them for residency benefits. It does not, at least not by virtue of ownership alone. What it does confer is a set of local commune tax obligations and national reporting requirements that demand careful attention.

The difference between a secondary residence and an investment property, whilst subtle, is pivotal. A property purchased purely for rental income with no personal use may attract a different fiscal treatment than one used partly by the owner and partly let to seasonal guests. French tax authorities observe the reality of occupancy, not merely the stated intent. Exploring the full spectrum of second home locations across the Var and Côte d’Azur reveals just how varied these classifications can become across communes.

Investors typically acquire secondary residences on the Riviera for a blend of the following purposes:

- Personal enjoyment and lifestyle enrichment, from Menton’s lemon-scented promenades during the Fête du Citron to Antibes’ Provençal market hauls at dawn

- Legacy and generational wealth transfer, structuring estates so that heirs inherit tangible, appreciating assets

- Retirement planning, securing a Riviera address well in advance of making it a primary residence

- Portfolio diversification, balancing financial instruments with bricks-and-mortar assets that historically appreciate 5 to 8 per cent annually on the Riviera

- Seasonal rental income, generating 3 to 5 per cent annual yields from elite short-term lets during the Cannes Film Festival, regattas, or Monaco Grand Prix season

Classification is not merely administrative. How your Riviera property is categorised by the local commune determines your taxe d’habitation liability, your eligibility for certain fiscal exemptions, and even the inheritance tax treatment your heirs will face. Treat this decision with the same rigour you apply to any blue-chip investment.

For those new to this landscape, consulting our buying a second home guide provides an authoritative starting point. Those with experience in UK real estate guidance will recognise parallels, though the French system carries its own distinct character.

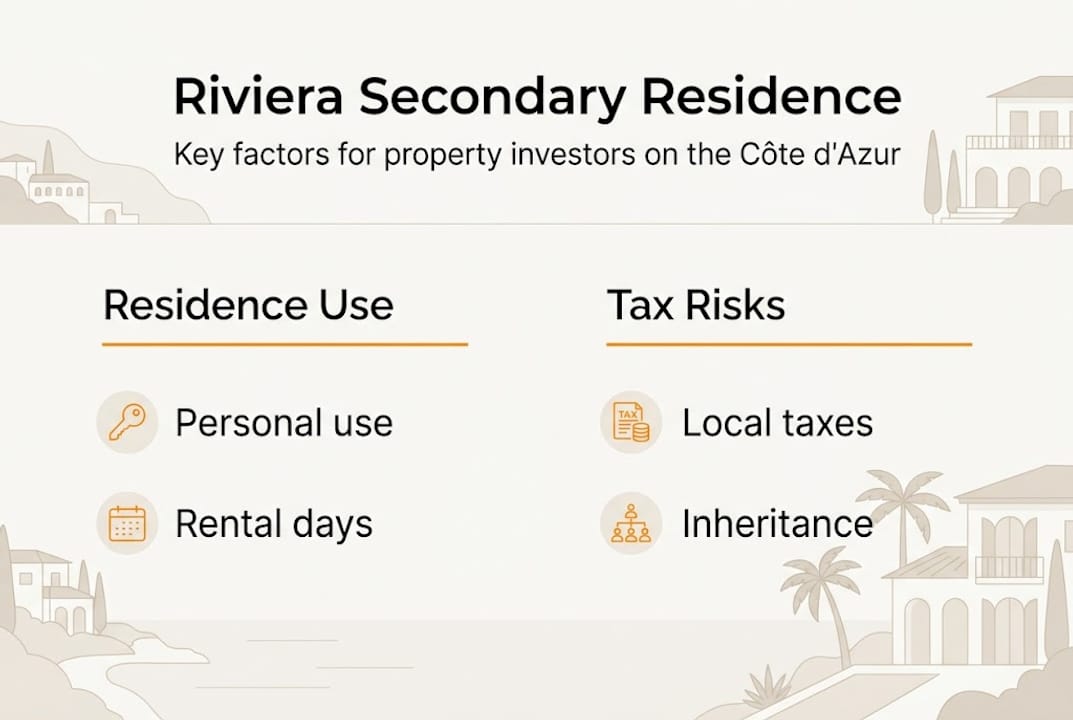

Personal use, rental, and tax categorisation: Navigating dual roles

Now, let us move from definitions to the practical mechanics of how your choices affect both your investment and your tax bill. The moment you introduce rental activity to a secondary residence, you alter its fiscal identity. This is not a theoretical concern; it is a lived reality for hundreds of Riviera property owners each season.

Shifting classification toward rental treatment can occur even when a property is used personally at certain times of the year. The French tax system, much like its Anglo-Saxon counterparts, is alert to properties that generate rental income while also functioning as personal retreats. The critical variable is proportionality: how many days is the property occupied by the owner, and how many days is it let commercially?

The practical consequences unfold as follows:

| Category | Occupancy criteria | Tax reporting requirement | Key risk |

|---|---|---|---|

| Personal use only | Owner-occupied throughout the year | Taxe d’habitation, taxe foncière declared annually | Surcharge risk in high-demand communes |

| Partial rental use | Mixed personal and rental days | Must declare rental income under BIC or micro-BIC regime | Misclassification triggers back tax |

| Predominantly rental | Minimal personal use | Full investment property treatment, TVA may apply | Loss of personal-use exemptions |

| Long-term lease | Property rarely personally used | Revenus fonciers regime, specific deductions apply | Excludes from certain capital gains reliefs |

When personal and rental days are tracked meticulously, investors can often preserve favourable tax treatment whilst still generating meaningful seasonal rental income. This dual role, personal sanctuary by spring and elite holiday let during the summer season when Pampelonne beach draws its glamorous crowds, is the model that most Riviera investors favour.

Pro Tip: Maintain a dedicated occupancy log from day one of ownership. Record every night the property is personally used and every rental period with its corresponding income. This log becomes your primary defence in any tax audit and your clearest evidence of legitimate personal use.

Legacy planning adds another layer of complexity. If a secondary residence is eventually intended for inheritance, the structure of ownership at the time of transfer determines the succession tax exposure. French inheritance law, governed by the Code Civil, applies forced heirship rules that can surprise international investors unfamiliar with the French system. Structuring ownership through an SCI (Société Civile Immobilière), a form of French property holding company, is one strategy that can facilitate smoother generational transfer whilst preserving the property’s status.

Reviewing our Riviera property tax guide and luxury real estate tax strategies will equip you with the detailed knowledge to navigate these obligations confidently. For additional visual context on the properties these strategies apply to, residential property visuals offer an evocative sense of scale.

French Riviera commune taxes: Local nuances every investor should know

With the importance of occupancy and rental categorisation clear, let us tackle the local tax rules that truly define your financial landscape on the Côte d’Azur. Three principal taxes apply to secondary residences in France, and all three have features that are particularly acute on the Riviera.

The taxe d’habitation on second homes is the most immediately relevant. Unlike primary residences, which were progressively relieved of this tax, secondary residences remain fully liable. Moreover, communes in high-demand zones, which describes virtually the entire coastline from Menton to Saint-Tropez, are legally permitted to apply a surcharge of up to 60 per cent on the base taxe d’habitation rate. The taxe foncière (property ownership tax) applies regardless of whether the property is occupied. Capital gains tax applies upon sale and diminishes progressively over time.

| Tax | Who pays | Rate range | Riviera surcharge risk |

|---|---|---|---|

| Taxe d’habitation | Owner of secondary residence | Varies by commune | Up to 60% surcharge in tension zones |

| Taxe foncière | Property owner | Varies, typically 0.5% to 1.5% of cadastral value | Moderate; less variable than habitation |

| Capital gains tax (plus-value) | Seller | 19% flat rate plus social levies (up to 36.2% total) | Reduced by exoneration after 22 or 30 years |

| IFI (Impôt sur la Fortune Immobilière) | Owners with net property assets above €1.3M | 0.5% to 1.5% progressive | Highly relevant for Riviera HNWI portfolios |

Several considerations shape how local tax rules influence investor decision-making:

- Location within the commune matters. A villa in Nice’s Mont Boron neighbourhood and one in a quieter inland village near Sainte-Maxime may carry very different taxe d’habitation liabilities, even if their market values are comparable

- Declared use is scrutinised. Communes have become increasingly rigorous in verifying that properties classified as primary residences genuinely meet the criteria, protecting secondary residence tax revenues

- IFI (Impôt sur la Fortune Immobilière) thresholds are particularly relevant on the Riviera, where a single sea-view villa can push an investor’s net property wealth above the €1.3 million trigger point

- Capital gains exoneration rewards long-term holding. After 22 years, income tax on capital gains is eliminated; full social levy relief arrives after 30 years, making patience a genuine strategy

Strategies for minimising tax liability across legacy properties include holding through an SCI, staggering sales across tax years, and timing disposals to maximise exoneration relief. Our Riviera real estate investor tax guide provides current 2026 guidance on each of these approaches, and our capital gains taxes overview clarifies the sale-stage implications. For comparative context, property tax in the UK illustrates how different fiscal architectures can be across jurisdictions.

Acquisition strategies for secondary residences: Personal enjoyment and legacy investment

Now let us put these principles into action and explore how investors approach acquisition for both pleasure and legacy. The French Riviera in 2026 presents three primary acquisition pathways: direct purchase of existing properties, investment in new off-plan developments, and access to curated off-market opportunities.

Each pathway carries its own blend of lifestyle appeal and fiscal consequence. A restored Provençal mas near Antibes, with shuttered windows opening onto terraced gardens heavy with bougainvillea, brings immediate character and a fully known tax history. A new development at Sainte-Maxime, steps from Nartelle beach with views across to Saint-Tropez, offers a ten-year structural warranty, lower notary fees typically around 2 to 3 per cent versus 7 to 8 per cent for existing properties, and often a staged payment plan that preserves capital liquidity during construction.

The sequential process for acquiring a secondary residence on the Riviera typically unfolds as follows:

- Define your dual mandate. Clarify the balance between personal enjoyment (seasonal presence, lifestyle access to Cannes regattas, Menton’s Lemon Festival) and investment objectives (rental yield targets, capital appreciation horizon, legacy structuring)

- Engage a specialist adviser. Appoint both a French notaire and an independent tax adviser familiar with international clients before viewing a single property

- Conduct legal and technical due diligence. Commission a titre de propriété audit, a structural survey, and where applicable a seismic resilience assessment

- Assess commune-level tax exposure. Request a detailed breakdown of current taxe d’habitation, taxe foncière, and any applicable surcharges for the specific property address

- Structure ownership correctly from the outset. Decide whether individual ownership, joint ownership, SCI, or an international holding structure best serves your legacy and tax goals before signing the compromis de vente

- Plan for generational transfer. Incorporate succession provisions into the ownership structure at the point of acquisition, not as an afterthought years later

The advantages of buying existing property on the French Riviera are considerable, particularly for investors who prize immediate occupancy and established rental track records. Equally, the benefits of buying a new home in the south of France are compelling for those who prize modern energy performance, biophilic design, and the clean slate of a property whose entire fiscal history you control from day one.

Pro Tip: Integrate your property selection with your long-term legacy and tax strategy from the first viewing. A villa that suits your lifestyle perfectly but sits in a commune with a 60 per cent taxe d’habitation surcharge may erode the net legacy value you intend to pass to your heirs. Profitability and pleasure must align. Drone property views can help you appreciate scale and position before committing to travel.

Second home locations across the Var and Côte d’Azur each carry their own micro-climate of tax risk, lifestyle reward, and legacy potential. The investor who treats location as a tax decision, not merely an aesthetic one, invariably makes the stronger acquisition.

A fresh perspective: Redefining secondary residence for legacy investors

We observe, across many years of working with global high-net-worth clients on the Côte d’Azur, a persistent and costly misconception. Investors arrive thinking of their Riviera property as a maison de vacances, a beautiful indulgence sitting apart from their serious portfolio. This framing is, we believe, the single greatest missed opportunity in Riviera real estate.

The secondary residence, when conceived as a legacy instrument from the very moment of acquisition, transforms entirely. Tax optimisation through occupancy management, carefully structured SCI ownership, and commune-level fiscal planning are not bureaucratic burdens. They are the levers that convert a holiday address into a generational asset. We have guided clients whose French Riviera investment strategy began with a single sea-view apartment and grew, through disciplined repositioning, into portfolios yielding both income and enduring family wealth.

The investors who thrive here are those who ask, from the first day of ownership: “How will this stone serve my heirs?” That question changes everything.

Explore luxury Riviera real estate opportunities

Having challenged traditional definitions and explored actionable strategies, here is how to make your next move on the Riviera with confidence. At Living on the Côte d’Azur, we curate an exclusive portfolio of Riviera villas and penthouses tailored precisely for investors who seek both personal opulence and enduring legacy value. Our team specialises in aligning lifestyle aspiration with fiscal intelligence, ensuring every acquisition serves your generational vision. From legacy real estate strategies to the art of curating high-value property in the most coveted communes, we are your trusted partner from first enquiry to final deed. We also accept cryptocurrency payments, because your wealth moves at the speed of the modern world.

Frequently asked questions

What legally defines a secondary residence in France?

A secondary residence is any property you own or occupy that is not your principal habitation, making it subject to distinct tax and commune rules including taxe d’habitation and specific reporting obligations.

How does rental use affect secondary residence tax treatment?

Rental use can shift classification towards an investment asset treatment, altering income reporting requirements and potentially reducing access to personal-use capital gains reliefs.

What is taxe d’habitation and who pays it?

Taxe d’habitation is a local property tax that remains fully applicable to secondary residences, with commune-level surcharges of up to 60 per cent possible in high-demand Riviera zones; the property owner bears this liability.

How do you optimise legacy planning with a secondary residence?

Optimising legacy planning requires structuring ownership correctly at the point of acquisition, whether through an SCI or another vehicle, tracking occupancy diligently, and aligning the property’s fiscal profile with your intended generational wealth transfer strategy.

Recommended

//

//