TL;DR:

- Paris property prices have stabilized at around €9,650 per square meter after an 8% correction from the 2020 peak, creating a buying opportunity. Mortgage rates have improved to the low 3% range, enhancing purchasing power for long-term investors.

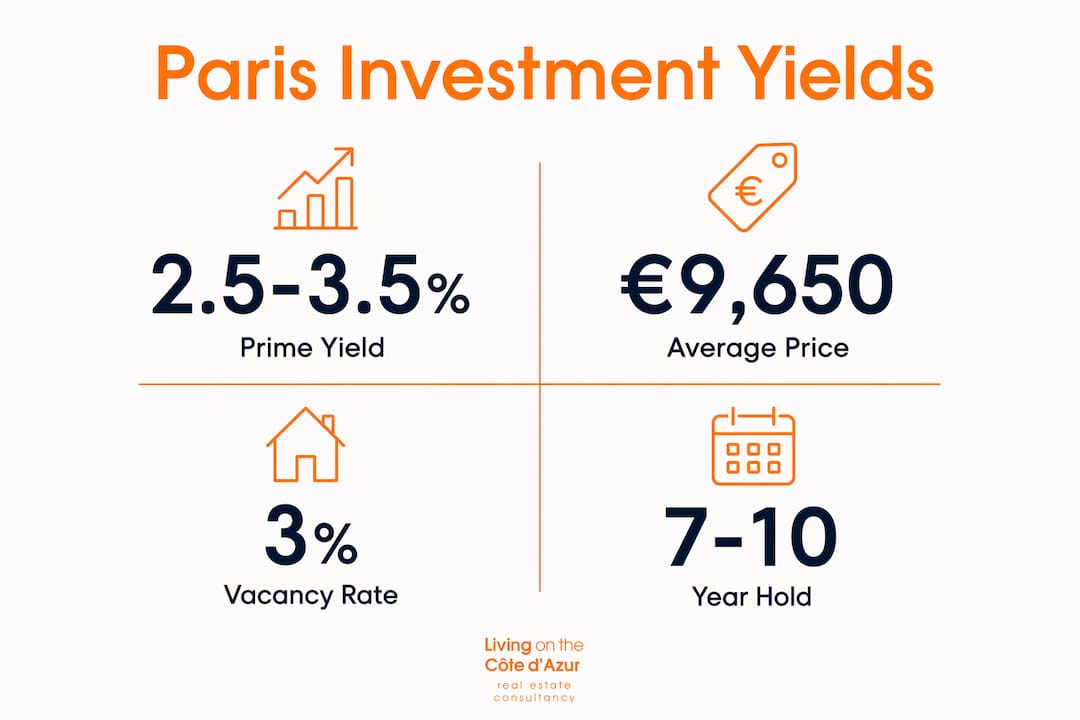

Paris property investment is defined by one compelling truth: the city’s apartment prices have stabilised at around €9,650 per square metre following an approximate 8% correction from the 2020 peak, creating a rare window of opportunity for discerning international buyers. Mortgage rates have improved to the low 3% range, restoring purchasing power that was eroded during the rate spike of 2023. The question of why buy in Paris 2025 is answered by this precise convergence of corrected prices, accessible financing, and a city whose prestige and scarcity of prime property have never diminished. For those with a long-term vision, the conditions today are among the most favourable seen in a decade.

Why buy in Paris 2025: what the market data reveals

The Paris real estate market in 2025 is best understood as a buyer’s market emerging from correction. Prices fell from their 2020 peak by approximately 8%, and that correction has now largely run its course. What remains is a market where sellers have adjusted expectations and buyers hold genuine negotiating power.

Price correction and what it means for you

Sales prices in 2025 typically settled 3–6% below asking prices. That figure is not trivial. On a €700,000 apartment in the 9th arrondissement, a 5% discount represents €35,000 returned to your pocket before you have even unpacked. The market is balanced to mildly buyer-leaning, which is precisely the environment where considered offers are accepted rather than dismissed.

Transaction volumes are also recovering. Average sale times in Paris ran at 68–82 days in 2025, faster than the sluggish correction period but still measured enough to allow due diligence. That pace signals a functional market, not a frenzied one. Buyers are not competing blindly; they are negotiating thoughtfully.

Key market conditions at a glance

- Price level: Stabilised at approximately €9,650/m² city-wide average

- Correction depth: Approximately 8% below the 2020 peak

- Negotiation room: 3–6% below asking price in most transactions

- Average sale time: 68–82 days, indicating a balanced market

- Mortgage rates: Settled in the low 3% range for 20-year fixed loans

- Transaction volume: Rebounding, with buyer confidence returning

Pro Tip: Time your offer during the autumn window, from September through November, when seller motivation tends to peak and competition from other buyers is lower than in the spring market.

The FNAIM projections indicate steady capital appreciation through 2026, outperforming broader French averages. That trajectory rewards those who act during the stabilisation phase rather than waiting for confirmation that prices have risen again.

Which Paris arrondissements offer the best investment value?

Price variation across Paris is dramatic, and understanding it is the foundation of any sound acquisition strategy. The city is not one market. It is twenty arrondissements with distinct characters, price points, and investment profiles.

Arrondissement price and yield comparison

| Arrondissement | Price range (€/m²) | Gross rental yield | Demand profile |

|---|---|---|---|

| 6th and 7th (Saint-Germain, Invalides) | 14,000–16,000 | 2.0–2.5% | Ultra-prime, capital preservation |

| 1st and 4th (Marais, Louvre) | 12,000–14,000 | 2.2–2.8% | Prestige, short-let demand |

| 9th and 10th (Opéra, République) | 9,000–11,000 | 2.8–3.2% | Strong rental demand, mixed profile |

| 11th and 12th (Bastille, Nation) | 8,500–10,000 | 3.0–3.5% | Young professional tenants, good liquidity |

| 19th and 20th (Belleville, Père Lachaise) | 7,000–8,500 | 3.2–3.5% | Emerging, value-driven entry point |

Rental yields in prime areas typically run at 2.5–3.5% gross and 1.5–2.5% net after costs. Paris is not a cash-flow market. It is a capital appreciation and wealth preservation market, and the distinction matters enormously when setting your expectations.

What drives enduring value in a Paris apartment

Location within an arrondissement matters as much as the arrondissement itself. Proximity to a Métro line, a covered market, and a well-regarded school catchment area all add measurable value. In the historic Haussmannian buildings that define the city’s character, floor level and lift access command premiums exceeding 10% over lower floors without a lift. A fourth-floor apartment with a lift in a well-maintained Haussmannian building on a tree-lined boulevard is not the same asset as a ground-floor flat on a commercial street, even if both carry the same postcode.

Vacancy rates below 3% in desirable areas confirm that rental demand is sustained by students, expatriates, and corporate tenants. That structural demand does not evaporate with economic cycles. Paris attracts a permanent population of internationally mobile professionals who require quality rental accommodation year-round.

Pro Tip: Prioritise well-located 2 to 3 room apartments with a DPE energy rating of C or above. French regulations are tightening on energy performance, and properties rated F or G face letting restrictions that will erode both rental income and resale value.

How do mortgage rates in 2025 affect your buying power in Paris?

Financing conditions are a central reason why investing in Paris real estate makes compelling sense right now. Mortgage rates decreased from above 4% in 2023 to approximately 3.1–3.3% for 20-year fixed loans by early 2026. That shift is not cosmetic. On a €600,000 mortgage, the difference between 4.2% and 3.2% over 20 years represents tens of thousands of euros in total interest paid.

What improved rates mean in practice

The monthly repayment on a €600,000 loan at 4.2% over 20 years is approximately €3,700. At 3.2%, that falls to roughly €3,400. The saving of €300 per month compounds to over €72,000 across the loan term. For buyers who were priced out in 2023, the current rate environment reopens the market at a meaningful level.

For international buyers, the financing process carries additional steps. French banks typically require:

- Proof of income from the past two to three years, including tax returns from your country of residence

- A deposit of 20–30% for non-resident buyers, though this varies by lender and nationality

- Life assurance linked to the mortgage, which is standard in France and adds a modest cost

- A French bank account, which most lenders require before completing a mortgage application

The long-term holding horizon of 7–10 years is the critical planning assumption. Transaction costs in Paris are substantial, and a short holding period will not allow appreciation to absorb them. Buyers who commit to a decade-long ownership horizon are the ones who consistently realise the market’s wealth-building potential.

Pro Tip: Engage a French mortgage broker who specialises in non-resident clients before you begin your property search. Pre-approval clarifies your budget and signals seriousness to sellers in a market where cash buyers are common.

What are the real benefits and challenges of buying Paris property?

Paris property is primarily a wealth preservation market, not a high-yield rental vehicle. Understanding that distinction protects you from misaligned expectations and positions you to extract the genuine value the city offers.

The case for Paris as a long-term investment

The benefits are structural and enduring. Paris has a finite supply of prestige property within the périphérique. New construction is limited by heritage protections, planning restrictions, and the sheer density of the existing urban fabric. That scarcity underpins long-term value in a way that no amount of market correction can permanently erode.

French tax structures offer international buyers meaningful advantages. The LMNP (Loueur en Meublé Non Professionnel) status allows depreciation deductions against rental income, reducing taxable yield significantly. The family SCI (Société Civile Immobilière) structure facilitates inter-generational wealth transmission with favourable inheritance tax treatment. France’s tax system is mature, transparent, and well-documented, which gives international buyers the confidence to plan across generations. You can read more about French capital gains tax to understand how disposals are treated over time.

Challenges to plan for honestly

The acquisition cost structure demands respect. Notary fees and transfer taxes add approximately 7–8% to the total acquisition cost. On a €500,000 apartment, that means budgeting an additional €35,000–€40,000 beyond the purchase price. Round-trip costs, including eventual sale fees, can reach €50,000–€65,000 on that same asset. These are not hidden costs, but they are costs that require a long holding period to justify.

| Challenge | Practical implication |

|---|---|

| Transaction costs of 7–8% | Plan a minimum 7–10 year hold to absorb acquisition costs |

| Limited new construction | Competition for quality stock in prime areas remains intense |

| Energy performance regulations | Avoid properties rated F or G under the DPE system |

| Non-resident financing complexity | Allow 3–4 months for mortgage approval as an international buyer |

| Rental yield below 3.5% net | Position the investment as capital appreciation, not income |

The recommended holding period of 7–10 years is not a suggestion. It is the minimum timeframe for the mathematics of Paris property to work in your favour. Buyers who enter with a short-term trading mentality consistently underperform those who treat Paris as a generational asset.

Key takeaways

Paris in 2025 is a wealth preservation market where corrected prices, improved financing, and structural scarcity combine to reward patient, well-informed international buyers.

| Point | Details |

|---|---|

| Prices have corrected and stabilised | At approximately €9,650/m², Paris offers the best entry point since the 2020 peak. |

| Mortgage rates improve affordability | Rates at 3.1–3.3% restore purchasing power lost during the 2023 rate spike. |

| Negotiation room exists | Buyers are achieving 3–6% below asking price in a balanced market. |

| Transaction costs require a long hold | Budget 7–8% in acquisition costs and plan a 7–10 year ownership horizon. |

| Tax structures reward planning | LMNP and SCI structures offer depreciation benefits and legacy wealth transmission. |

Paris in 2025: my honest assessment after years in the market

By Ab Kuijer

I have watched clients hesitate at precisely the wrong moments. They waited for certainty in 2021, when prices were at their peak, because the market felt safe. They hesitated again in 2023, when rates rose and sentiment turned, because the market felt uncertain. The buyers who acted in both those periods with clear strategy did well. The ones who waited for a perfect signal are still waiting.

Paris in 2025 is not a perfect market. No market is. But it is a market where the conditions align in a way I find genuinely compelling for international buyers with a long-term horizon. The price correction has done its work. Sellers have recalibrated. Financing is accessible again. And the city itself, with its heritage protections, its cultural permanence, and its structural shortage of quality stock, has not changed.

What I tell clients who ask whether now is the right time is this: the right time is when the fundamentals support a long-term decision, not when the headlines feel comfortable. The headlines in Paris today are cautiously positive. The fundamentals are sound. The negotiating environment is the most favourable it has been in five years.

The one thing I would caution against is entering Paris with a yield-first mentality. If you need 5% net rental income to justify the acquisition, Paris will disappoint you. If you are building a portfolio of assets that will hold and grow value across a decade or more, Paris belongs in it. The city has absorbed wars, recessions, and pandemics. It has always recovered. That is not sentiment. That is history.

Choose your arrondissement with care, prioritise energy-efficient stock, and work with advisors who understand both the French legal framework and your personal wealth objectives. The property investment process in France rewards those who prepare thoroughly and act with conviction.

— Ab Kuijer

How Livingonthecotedazur supports your Paris acquisition

At Livingonthecotedazur, we work with high-net-worth individuals and families who approach property as a legacy asset, not a transaction. Our network spans over 100,000 properties across prestigious French locations, and our team brings the same rigorous, transparent Dutch approach to Paris acquisitions that has defined our work on the Côte d’Azur for years. We provide legal audit support, tax optimisation guidance including LMNP and SCI structures, and financing assistance tailored to international buyers. Whether you are seeking a prestige pied-à-terre in the 6th arrondissement or a well-located investment apartment in the 11th, we connect you with the right property and the right advisers. Explore our curated selection of off-market luxury properties and discover what becomes possible when expertise meets exclusivity.

FAQ

What is the average price per square metre in Paris in 2025?

Paris apartment prices stabilised at around €9,650/m² in early 2026, approximately 8% below the 2020 peak. Prices range from €7,000–€8,500/m² in outer arrondissements such as the 19th and 20th to €14,000–€16,000/m² in prestigious central districts like the 6th and 7th.

Is Paris a good investment in 2025 for international buyers?

Paris is a strong wealth preservation investment for buyers with a 7–10 year holding horizon. Capital appreciation prospects are solid, FNAIM projects steady price growth outperforming broader French averages, and structural scarcity of prime stock underpins long-term value.

What mortgage rates are available for Paris property in 2025?

Fixed 20-year mortgage rates settled in the 3.1–3.3% range in 2025 and early 2026, down from above 4% in 2023. International buyers typically require a 20–30% deposit and should allow 3–4 months for the approval process with a French lender.

How much should I budget for transaction costs when buying in Paris?

Transaction costs including notary fees and transfer taxes add approximately 7–8% to the acquisition price. On a €500,000 purchase, that means budgeting an additional €35,000–€40,000, with full round-trip costs potentially reaching €50,000–€65,000.

What tax structures are available to international buyers in Paris?

France offers the LMNP status for furnished rental properties, allowing depreciation deductions against rental income. The family SCI structure facilitates inter-generational wealth transmission with favourable inheritance tax treatment. Both structures are well-established and accessible to non-resident buyers with proper legal guidance.

Recommended

//

//